AI promises efficiency – but scaling it depends on disciplined sourcing and vendor orchestration

Scaling AI while Managing Margin and Opex Pressure

Tech Sourcing in TMT

Tech Sourcing in TMT

For telecom and media operators, technology is no longer a support function, it is the product. Networks, platforms, cloud infrastructure and AI capabilities directly shape customer experience, cost structure and growth potential.

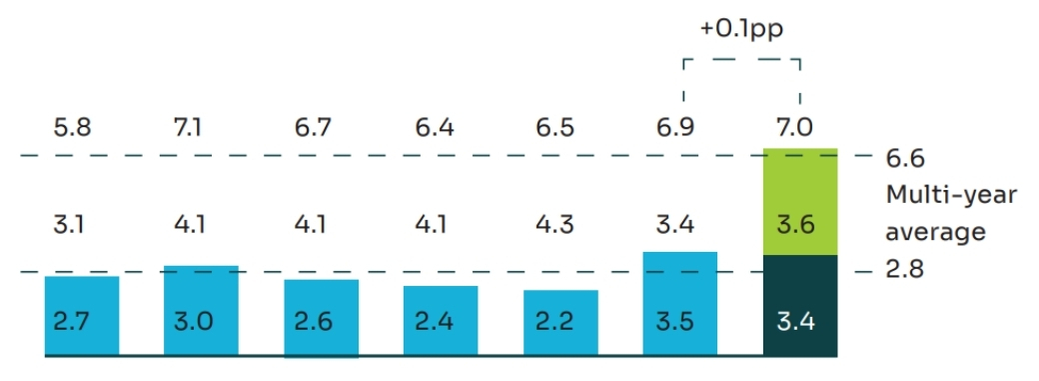

Yet financial momentum remains limited. Median revenue growth among operators stands at roughly 2%, while EBITDA margins remain under pressure. At the same time, IT spending continues to rise and now averages around 7% of revenues. Investment is accelerating, but margin expansion is not. The result is a structural tension: operators are investing heavily in digital capabilities and AI, but margin expansion remains elusiv

What fundamentally changes the equation is the shift in cost structure. Technology spending is steadily moving from capital expenditure toward recurring operational expenditure. In an opex-heavy model inefficiencies are no longer absorbed over time, they hit the income statement immediately. Cloud services, SaaS platforms, managed services and hyperscaler contracts create recurring cost exposure that directly shapes EBITDA performance.

This structural shift elevates tech sourcing from a cost-control function to a margin management instrument. Vendor strategy now determines profitability in real time. Contract design, consumption governance and sourcing discipline directly influence financial resilience.

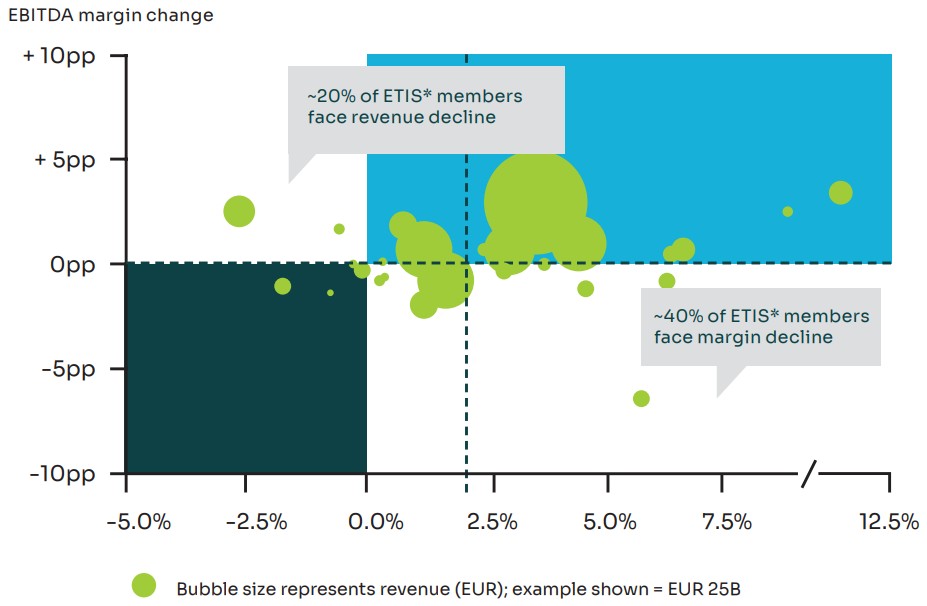

Telco’s financial performance remains broadly stable, with modest revenue growth (~2%) and limited margin improvement. Fewer than half of operators achieved both revenue and margin growth.

Source: BCG TeBIT 2025

Less than half of ETIS* members achieved both margin and revenue growth–demonstrating the need for

Source: BCG TeBIT 2025

The shift toward opex-heavy IT spending increases the immediate margin impact of sourcing decisions.

AI and generative AI are widely recognized as key enablers of both growth and efficiency. According to BCG’s TeBIT 2025 study, 53% of operators identify efficiency and productivity as the primary objective of AI adoption. Current applications span customer interaction automation, AI-assisted sales and service, predictive network maintenance, traffic optimization and advanced analytics.

Encouragingly, network spending as a share of revenue declined by approximately 4.1% in 2024, reflecting rollout completion and automation effects.

Yet while AI adoption is broad, scale remains uneven. Many operators continue to struggle with fragmented data landscapes, legacy system dependencies, immature toolchains and unclear ownership between IT, network and commercial functions.

AI promises efficiency – but scaling it depends on disciplined sourcing and vendor orchestration

// Business objectives of AI and GenAI

Efficiency and productivity rank as the primary AI objective among telcos. (% of responses)

Source: BCG TeBIT 2025

As operators invest in AI foundations – architecture, cloud, data platforms – the sourcing implications become unavoidable. Decisions on whether to build capabilities internally or leverage vendor ecosystems determine both cost trajectory and innovation speed. Hyperscaler concentration risk, platform dependency and AI tooling choices directly influence long-term margin dynamics.

In an ecosystem shaped by global platform providers and OSS/BSS vendors, procurement decisions no longer only affect cost levels, they shape competitive positioning.

In TMT, tech sourcing increasingly defines competitive position. Cost excellence remains the foundation. Structured negotiations, demand discipline, automation and portfolio rationalization can unlock significant efficiency potential in IT services and network operations. Benchmarks suggest 15–25% savings potential in selected categories when levers are applied systematically.

But the differentiator lies beyond cost. Many operators now generate close to one-third of revenues from beyond-core services such as ICT solutions, cloud offerings, digital content ecosystems and data-driven platforms. Vendor selection therefore directly influences product portfolios, monetization models and customer experience.

Leading operators treat procurement not as a transactional function, but as a strategic lever across three dimensions:

Vendor Portfolio Discipline

Clear build-versuspartner boundaries and active management of hyperscaler and platform concentration risk.

Innovation Alignment

Sourcing strategies that align with AI roadmaps, data platforms and digital product strategies.

Operating Model Integration

Governance structures that link procurement, IT, network and commercial leadership – ensuring that sourcing supports both margin discipline and innovation speed.

Recent industry perspectives emphasize that operators who treat procurement as a strategic function – rather than a transactional one – outperform peers in balancing growth and efficiency.

Managing Director

Principal