Portfolio companies experienced a significant increase in value in the first five years after being acquired.

// SMI 06 | Cost Optimization – How to get a fresh start

Private equity firms have long been seen as ruthless profit-seekers who are rarely interested in developing their portfolio of companies in the long-term. They may be derided as profit-seekers, but it seems that these financiers still create opportunities. Our desk research into the performance of portfolio companies proves that they significantly outperform their competitors without private equity involvement.

German politician Franz Müntefering of the Social Democratic Party lamented in an interview in April 2005 that: “Some financial investors never think about the people whose workplaces they destroy – they remain anonymous, faceless, descend like swarms of locusts on companies, strip them bare and then move on again.”

They still have their critics, even today – for example, in the study published in January by the Hans Böckler Foundation on how companies owned by private equity firms develop in Germany, which focused on the negative trend of equity capital ratios and number of employees at multiple companies across all industries that had been bought by private equity firms since 2013.

We have found that these results do not apply to portfolio companies in the industrial goods or process industries, as they experienced a significant increase in value in the first five years after being acquired. Portfolio companies achieve more than twice the EBITDA and revenue growth compared to companies from these industries without PE participation.

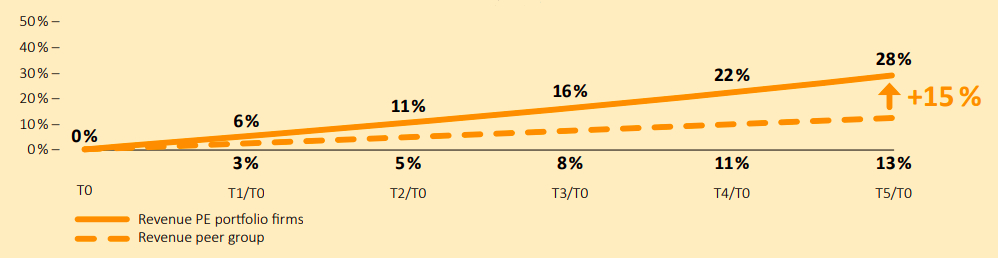

This observation applies across the full five years and the gap widens from year to year. For example, the sales of portfolio companies grow by an average of 28 percent during the period under review, while companies without PE participation achieve 13 percent. The difference for operating profit (EBITDA) is even graver, with portfolio companies achieving 42% growth and other companies having to settle for 9%.

If we compare the number of employees, here, too, the portfolio companies are ahead: their headcount is growing faster than that of their sector peer group, at 12 percent compared with nine percent. The only time we saw staffing levels fall was when we restricted the analysis parameters to portfolio companies where the focus was purely on restructuring.

// Revenue Development: PE Portfolio Firms vs. Peers

Portfolio companies in ‘Industrial Goods’ and ‘Process Industry’ perform strong compared to the industry peer group with +15%-points revenue

// EBITA & Operational Cost Development: PE Portfolio Firms

Portfolio companies experienced a significant increase in value in the first five years after being acquired.

If companies want to increase their operating profit, they don’t need to be taken over by a private equity firm before launching optimization projects. However, the significantly better results from portfolio companies do demonstrate that applying their strategies will pay off. Below are some examples of promising approaches to reduce costs in the long-term:

We can see notable differences within portfolio companies when it comes to material costs. On average, the material costs per unit produced remain stable, while the most successful portfolio companies achieve a growth in EBITDA of 94% by also reducing their material costs on an ongoing basis – by up to 8% within five years.

Private equity firms drive cost optimization to create a sustained increase in value across their portfolio companies. The most successful ones take innovative and complex approaches to procurement, while also investing in digital solutions such as analytics tools and process automation.

For our analysis, we examined annual reports of 67 portfolio companies from 2013 to 2019. We compared the trends in companies from the industrial goods and process industries with those of companies from these industries that were not owned by private equity firms.

Most portfolio companies are based in Europe (a total of 89%), with the majority in Germany, France, and the United Kingdom (45% combined). We also looked at companies in Canada and the USA (11%). The peer group data comes from public and private statistics providers. Of the portfolio companies we examined, 56% are pursuing a growth course, while 44% are implementing a restructuring program.

Looking at the industrial goods and process industries, our long-term analysis indicates that mistrust in private equity firms is largely unfounded. As our figures show, many private equity firms tend to take a long-term approach and are focused on sustainable business success. The challenges of the coronavirus pandemic have hit companies hard, so they are on the lookout for investors. At the same time, private equity firms have significant amounts of capital at their disposal (referred to as dry powder), creating promising opportunities for both sides.

Torben Alhusen

Principal