China’s export controls on rare earth elements (REEs), and particularly rare earth magnets, have reshaped global supply chains across sectors ranging from consumer electronics to defence and automotive. This reflects China’s overwhelming dominance of REE refining and production of rare earth magnets, which are key components in myriad devices.

Companies that depend on these inputs face delays in obtaining export licenses and uncertainty over the evolving rules. And while finished components that incorporate rare earth magnets can be exported from China without a license, they face tariffs on entry to the US.

-

This microsite outlines a five-step playbook for procurement leaders to guide their organizations through short-term disruptions. It then offers three strategic steps to future-proof supply chains for a new era of uncertain access to critical inputs.

The Structural Bottleneck: Rare Earth Magnets

Maintaining access to rare earths elements (REEs) is arguably the biggest challenge to industrial supply chains today. In April 2025, China, which dominates global production of REEs, introduced export controls on a group of these essential materials. This directly affected manufacturers of everything from EV motors to MRI scanners, wind turbines to fighter jets, smartphones to machine tools.

Until this moment, global manufacturing’s dependence on China for supplies of REEs was under-appreciated. That has rapidly changed. China’s export controls coupled with rising US import tariffs and evolving EU industrial policies have exposed just how fragile industrial supply chains are, with automakers and electronics manufacturers warning of delays and uncertainty over export rules.

The episode holds a stark lesson for boards everywhere: despite their efforts to diversify manufacturing footprints, the flow of key materials still depends on China, which dominates REE refining and the production of essential intermediate products such as rare earth magnets, which are required in a huge variety of finished products.

While companies often react to visible short-term disruptions, structural material dependencies tend to receive less attention until access is directly constrained. Rare earth elements exemplify this dynamic: the strategic exposure has existed for years, but only recent regulatory shifts have made it fully visible.

Despite their name, the 17 metallic elements collectively known as rare earths are found in many parts of the world – new mines are opening in the US, Australia and Africa. But the challenge isn’t finding REEs, it’s refining them. Turning mined material into usable industrial inputs requires large-scale chemical separation and processing plants that are both expensive and environmentally damaging. China has invested heavily over decades to build the refining capacity and technical expertise that the world now relies on. As a result, diversifying downstream manufacturing operations away from China does not eliminate exposure, because the upstream bottleneck remains. Similarly, diversification of extraction sources must be accompanied by diversification of refining and processing capabilities. Without parallel investment in separation capacity and magnet production, mining diversification alone does not materially reduce systemic dependency.

For procurement leaders, the question is no longer whether supply will tighten. It is how to mitigate critical dependencies and de-risk supply chains. Success will require a new mindset: one that treats rare-earth sourcing not as a purchasing exercise but as a strategic capability built on visibility, collaboration and planning.

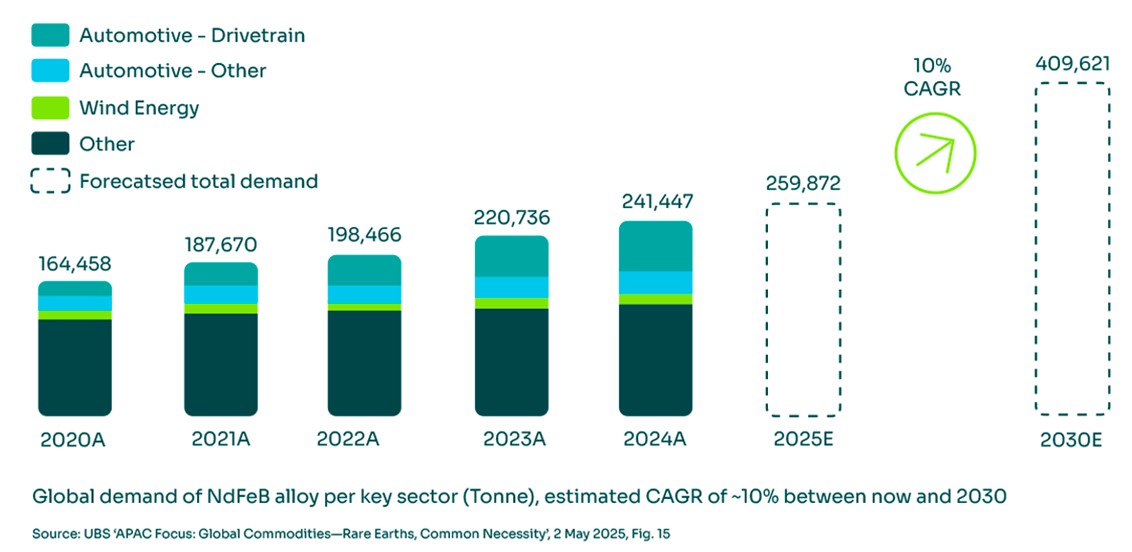

Among the many applications of REEs, one of the most important is Neodymium-Iron-Boron (NdFeB) permanent magnets. These are used in a huge range of manufacturing industries as indicated above. Global demand for NdFeB magnets is projected to grow at roughly 10% CAGR through 2030, with automotive and wind energy accounting for most of that increase. Ensuring continuity of supply is therefore essential.

// Global NdFeB Alloy Demand

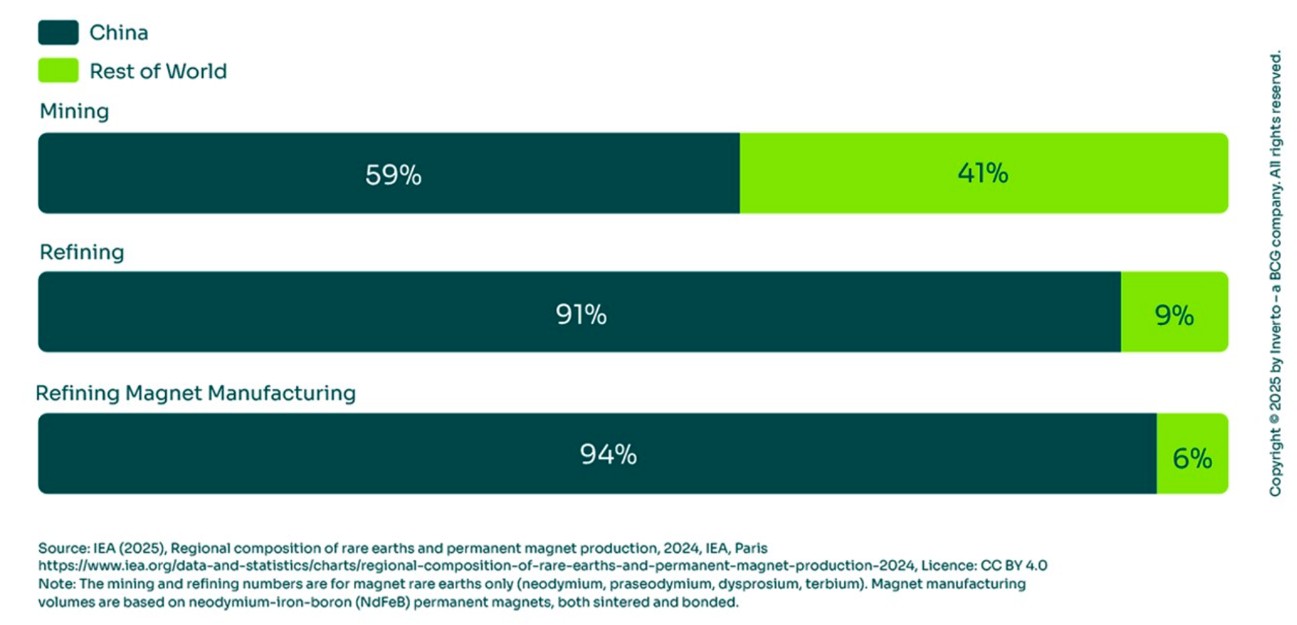

China dominates the value chain for rare earth magnets, accounting for more than 90% of both refining capacity and magnet block production. It also dominates production of magnet-making equipment, such as sintering and plating machines. This concentration reflects huge investment and accumulated know-how that cannot be replicated quickly.

// Rare Earth Magnet value chain share (2024)

The result is a critical dependency. Even relatively small policy or regulatory changes can ripple across global industries, leading to supply delays, price volatility and compliance uncertainty.

Tariffs & Export Controls: From Cost Risk to Access Risk

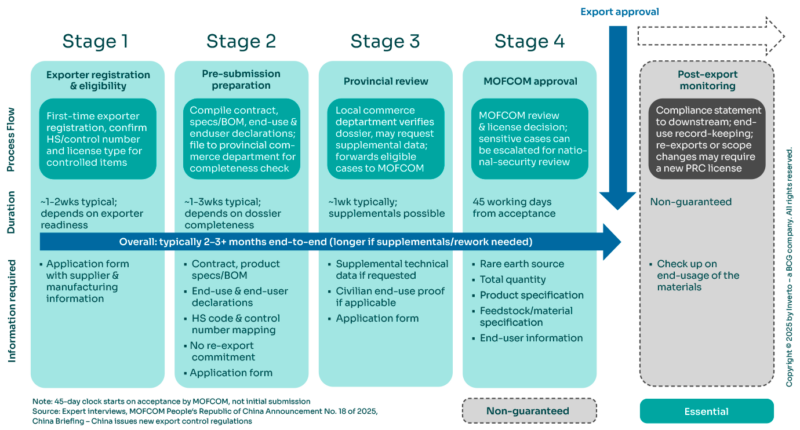

In April 2025, shortly after the US announced increased tariffs, China’s Ministry of Commerce (MOFCOM) and General Administration of Customs (GAC) introduced new export controls on seven medium and heavy rare earth elements – Dysprosium, Terbium, Samarium, Gadolinium, Yttrium, Lutetium and Scandium. These rules cover exports of processed REEs, rare earth magnet blocks, finished magnets and key magnet-making equipment. Each export now requires a license obtained after a multi-stage review process.

While the stated target for processing license applications is 45 days, approvals often take longer, and requests for additional documentation can further delay the process. Applications undergo close scrutiny of declared end uses and upstream process chains, and once approved, licenses are temporary and quantity-specific, typically valid only for a few months. As a result, suppliers must reapply continuously to maintain export continuity.

These controls have increased the timing risk for cross-border supply chains, thanks to the extra time required since April to obtain export approvals.

In October 2025, China announced plans to extend export controls to five additional REEs although implementation was delayed for a year under a U.S.–China agreement.

In practice, however, enforcement of existing controls remains uneven, with boundaries between regulated and exempt materials frequently shifting as reviews evolve. These ongoing rule changes therefore increase compliance risk for manufacturers.

// China’s export licensing for REEs & magnets (2025)

These export controls illustrate how policy changes can reshape supply access faster than production capacity can adjust. They have turned REE sourcing from a question of cost and delivery into one of compliance and foresight – a dynamic that will define procurement strategy in the years ahead.

In response to rising geopolitical pressures, many companies have accelerated efforts to shift their manufacturing away from China. But because global REE refining and processing capacity is concentrated in China, international manufacturers remain dependent on Chinese inputs – shifting downstream operations abroad does not eliminate exposure, because the upstream bottleneck remains.

Alongside its imposition of export controls, however, China has confirmed that finished components that contain rare earth magnets remain remain exportable.

Companies that have continued to source finished components that contain rare earth magnets from China have faced fewer disruptions from export controls. However, US tariffs have introduced operational complexity for these companies.

- Tariffs and escalation of landed cost: Import duties such as US Section 301 measures and other trade measures significantly raise landed costs for imports. From Jan 2026, modifications to Section 301 further increase tariff exposure for permanent magnets imported from China

- Sole-source risk: Relying exclusively on Chinese finished goods concentrates exposure; if export rules are tightened further, these channels could close quickly.

- Market reaction: Benchmark neodymium prices rose by about 40% year-on-year (as of Oct 2025), reflecting tightening supply chain and export-related uncertainty.

To navigate between supply disruptions on one side and tariff pressures on the other, many organizations are adopting dual-sourcing approaches that combine:

- China-based sourcing for near-term continuity and export approval agility

- Regional or allied market suppliers – such as Lynas in Malaysia/Australia, MP Materials in the US or small but growing NdFeB capacity in Japan and Vietnam

- Direct raw-material agreements or recycling initiatives to reduce dependence on constrained upstream flows

While this hybrid approach introduces complexity, it offers resilience through flexibility. Procurement teams can pivot supply lines, manage cost tiers and adapt as policies, tariffs and market conditions evolve.

In the next section, we explore how procurement leaders can translate these strategies into action – embedding resilience across planning, operations contracting, and supplier management.

A Five-Step Stabilization Playbook for Procurement

Many teams assume they’re insulated from disruption because they source finished components from Tier 1 suppliers. But real exposure often lies two- or three-layers deeper – in the materials used, how they’re processed and where those steps occur.

Procurement teams should work to:

- Map not just suppliers, but full material and process flow, working with suppliers to trace material origin and identify choke points

- Flag steps tied to high-risk regions or controlled export categories

- Use supply chain risk dashboards and digital mapping tools to monitor exposure dynamically

This visibility exposes weak links before they break, enabling smarter mitigation and investment choices.

Knowing which SKUs use magnets isn’t enough. Procurement must collaborate with demand planning and engineering to estimate material-level requirements (e.g. monthly Dysprosium demand across programs). To make this actionable:

- Apply an Integrated Business Planning (IBP) framework to align procurement, demand and supply risk planning

- Use a criticality/impact framework to rank exposure: how essential the part is, and the business impact if it is unavailable – not only for REEs but also for other potential bottlenecks (e.g. semiconductors, specialty alloys)

- Prioritize allocation of constrained materials to the most business-critical programs and explore substitute specifications where possible

Effective mitigation requires visible cross-functional alignment — connecting procurement, engineering, compliance and executive leadership through a shared material-risk governance framework.

For suppliers reliant on restricted inputs, export licensing is now a major bottleneck. Procurement can:

- Assist with license documentation and consolidated volume forecasts

- Build in lead-time buffers and contingency plans for 60-90-day review cycles

- Track regulatory developments with legal/compliance partners to stay ahead of changes

These actions reduce friction and position procurement as a coordinator across legal, logistics and operations.

Procurement can also act to diversify material access and processing capacity by:

- Identifying regional suppliers with REE processing or magnet making capabilities (e.g. MP materials, Lynas, etc.)

- Engage with global brokers or partners who may hold , offering short-term relief

- Supporting recycling initiatives to recover usable REE content from older parts, engineering builds or post-production scrap

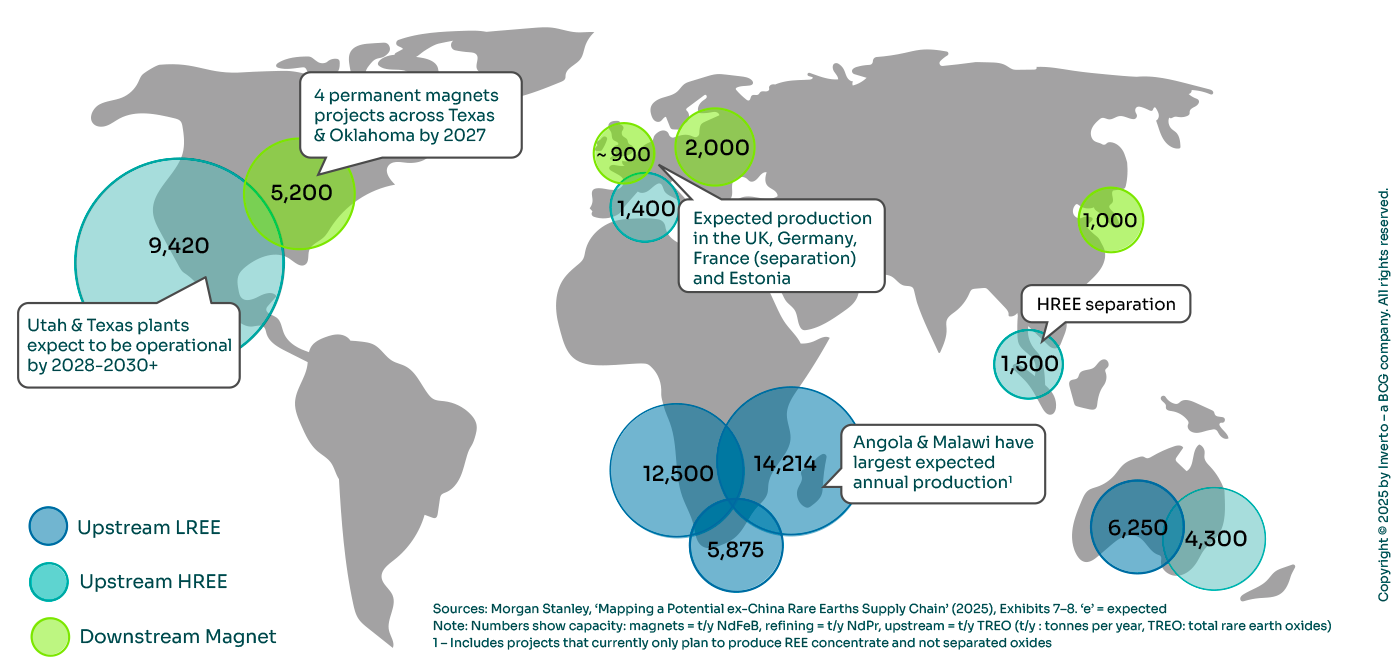

//Planned facilities across rare earth value chain

Notable planned rare earth facilities outside of China

The map above highlights planned rare-earth projects in markets such as Australia, the US, parts of Africa, etc. While new capacity is emerging, it remains small relative to global demand, underscoring how dependent the broader ecosystem still is on the established Asian supply chains.

Alongside operations and engineering, procurement can also help accelerate new supplier qualification or enable short-term production ramp-ups through flexible manufacturing strategies.

Procurement teams should revisit the structure of supplier agreements to ensure they support both short-term continuity and rapid pivoting when required. Key topics include:

- Volume flexibility – Allowing for scalable orders in response to license approvals or supply shortfalls

- Multi-site manufacturing terms – Enabling fulfillment from alternate geographies when regulatory conditions change

- Trigger-based clauses – Embedding pre-agreed thresholds (e.g. license not granted within X days) that activate a switch to alternative sourcing or adjusted terms

- Market-linked pricing – Tying REE pricing to public indices or tariff bands to reduce renegotiation needs during periods of cost volatility.

These mechanisms don’t just reduce friction: they help procurement teams act faster in moments of disruption, while also improving trust and alignment with suppliers.

Three Structural Moves to Future-Proof Rare Earth Procurement

Short-term actions can stabilize REE supply today, but long-term resilience requires a structural shift in how companies design, source and manage critical materials across the value chain. This applies at both the procurement level – in terms of contracts, supplier strategies and risk frameworks – and across the broader supply chain, where design choices and integration models shape long-term flexibility.

Three strategic steps underpin this transition:

Resilience begins long before sourcing decisions are executed. Once specifications are fixed, procurement’s ability to influence material risk is limited. Integrating procurement into concept development and stage-gate reviews ensures that exposure to high-risk materials is assessed alongside performance and cost from the outset.

Early involvement enables teams to flag magnet grades tied to Dysprosium or Terbium, evaluate availability trade-offs between alternative designs and build dual-sourcing or substitution pathways into the development process. Designing with supply constraints in mind is significantly less costly than retrofitting resilience after disruption occurs.

Design decisions can reduce exposure to policy or supply shocks over time. Companies are increasingly exploring:

- Rare-earth-reduced or magnet-free alternatives: Companies are investing in designs that use less Dysprosium and Terbium, or trialing non-REE motor architectures. While some of these remain in R&D, the trajectory is clear.

- Semi-knock-down (SKD) assembly models: In this approach, sub-assemblies containing magnets are sourced from China – falling outside the restricted categories – while final integration happens elsewhere. For example, a motor housing with magnets could be shipped from China, with final assembly completed in Vietnam (to benefit from lower tariffs) or the US (to avoid tariffs entirely). This structure can provide more consistent supply while maintaining compliance.

- Modular product platforms: Some OEMs are developing standardized motor designs that use fewer or no REE magnets that can scale across multiple platforms. Companies such as BMW are developing systems using externally excited synchronous (EESM) and asynchronous (ASM) motors as alternative building blocks. While this approach doesn’t allow “swapping” between REE and non-REE designs at will, it allows deployment of resilient alternatives more quickly and consistently across product families.

Rare earth disruption underscores a broader structural lesson: material exposure must be governed as systematically as financial or operational risk.

This means embedding geo-sensitive material tagging into sourcing systems, integrating raw material exposure reviews into category strategies and stage-gate processes, and continuously monitoring export controls, licensing regimes and tariff developments at the material – not just supplier – level.

Over time, this institutionalized visibility transforms procurement from a reactive escalation function into a strategic risk architect, capable of anticipating bottlenecks before they materialize.

Conclusion

Rare earth disruption reflects a structural shift in how material dependencies translate into industrial risk. It is redefining how procurement must operate. Stabilizing supply today is essential, but lasting resilience requires a structural shift: from reacting to constraints to deliberately designing flexibility into sourcing models, contracts and product decisions.

In this environment, procurement is no longer just safeguarding cost and continuity. It is becoming the architect of material resilience – shaping how organizations secure access to critical inputs in an era of geopolitical volatility.

Acknowledgements

We would like to thank Claire Mengxin Guo and Callum Phillipps for their valuable contributions and support in shaping the analysis.

The 17 Rare Earth Elements (REEs)

Rare earth elements comprise 15 lanthanides plus Scandium and Yttrium. They are commonly classified into Light Rare Earth Elements (LREEs) and Heavy Rare Earth Elements (HREEs).

| Element | Symbol | Category (LREE/HREE) | Primary Industrial Applications |

|---|---|---|---|

| Lanthanum | La | LREE | Catalysts, optics, batteries |

| Cerium | Ce | LREE | Catalysts, glass polishing, automotive catalytic converters |

| Praseodymium | Pr | LREE | Permanent magnets (NdPr blends), aerospace alloys |

| Neodymium | Nd | LREE | Core material in NdFeB permanent magnets |

| Promethium | Pm | LREE | Limited commercial use (radioisotope applications) |

| Samarium | Sm | LREE | Samarium-Cobalt (SmCo) magnets, aerospace systems |

| Europium | Eu | LREE | Phosphors, display technologies |

| Gadolinium | Gd | HREE | MRI contrast agents, nuclear applications |

| Terbium | Tb | HREE | Enhances magnet coercivity and heat resistance |

| Dysprosium | Dy | HREE | Improves thermal stability of NdFeB magnets |

| Holmium | Ho | HREE | Magnets, nuclear control rods |

| Erbium | Er | HREE | Fiber optics, lasers |

| Thulium | Tm | HREE | Medical lasers |

| Ytterbium | Yb | HREE | Electronics, specialty alloys |

| Lutetium | Lu | HREE | Medical imaging isotopes, catalysts |

| Yttrium | Y | HREE | Advanced ceramics, electronics, phosphors |

| Scandium | Sc | HREE | Lightweight aluminum alloys, aerospace applications |

Get in Touch

Justus Brinkmann

Justus Brinkmann

Principal

Stephane Crosnier

Stephane Crosnier

Managing Director

Ranjith Kumar Suresh

Ranjith Kumar Suresh

Project Manager

Gain deeper Insights